Market Scenario

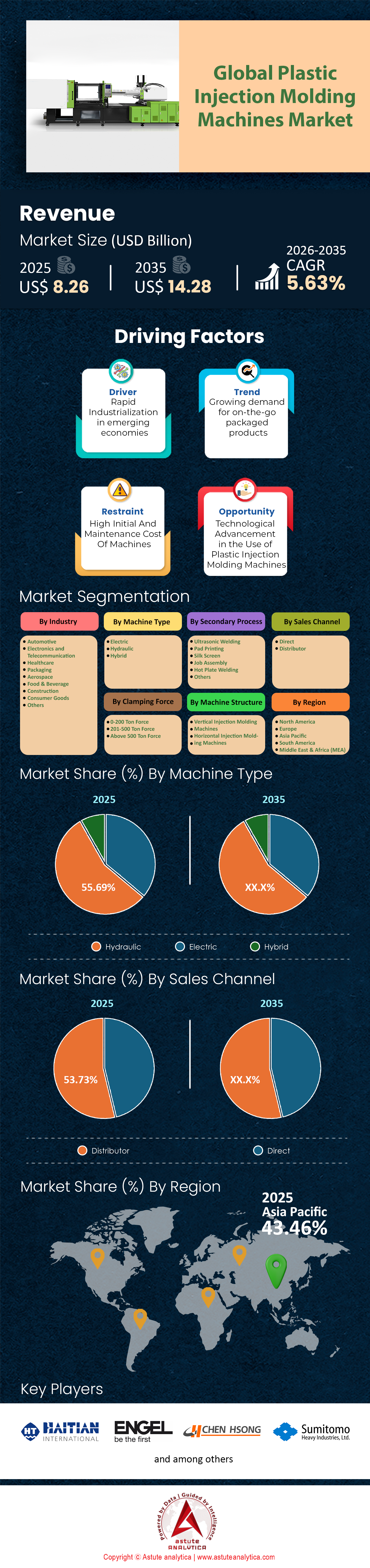

Plastic injection molding machines market was valued at US$ 8.26 billion in 2025 and is projected to hit the market valuation of US$ 14.28 billion by 2035 at a CAGR of 5.63% during the forecast period 2026–2035.

Key Market Highlights

- By machine type, hydraulic machines still have the stranglehold on the market.

- By clamping force, 201–500-ton force held more than 52.97% of the market.

- By machine structure, horizontal injection molding machines have solidified their spot-on top with a whopping 75.33% market revenue contribution.

- By industry, automotive industry has taken the lead in the plastic injection molding machines market by contributing more than 28.21% revenue.

- By Region, Asia Pacific controls the largest 43% market share.

The Plastic Injection Molding Machine (PIMM) market is no longer defined simply by "clamping force" or "shot weight." In 2025, the market has shifted from a hardware-centric industry to a software-defined manufacturing ecosystem.

For decades, the narrative was simple: Hydraulic for power, Electric for precision. That binary distinction has collapsed. The modern stakeholder is not just buying a machine, they are buying an energy-management platform. With global industrial electricity prices averaging 15–25% higher in 2025 than in 2021, the operational expenditure (OPEX) of molding equipment has superseded Capital Expenditure (CAPEX) as the primary decision driver.

The report on the plastic injection molding machines market analyzes the seismic shift caused by the convergence of three vectors: the aggressive electrification of machinery (driven by the EU Ecodesign Directive), the automotive transition to EV architectures (requiring massive, lightweight integrated parts), and the medical sector’s demand for cleanroom-ready micron precision. The market is already witnessing the phasing out of standard hydraulic toggles in favor of servo-hydraulic and all-electric units, even in high-tonnage applications previously thought immune to electrification.

To Get more Insights, Request A Free Sample

What Critical Four Market Trends Stakeholders in Plastic Injection Molding Machines Market Should Know Immediately?

- The "Crossover Point" Has Shifted: As of Q3 2025, the Total Cost of Ownership (TCO) crossover point—where an All-Electric machine becomes cheaper than a Hydraulic equivalent due to energy savings—has dropped from 3.5 years (2020) to 1.8 years.

- The 3,000-Ton EV Surge: There is a supply bottleneck for >3,000-ton two-platen machines. This is driven exclusively by the "Gigacasting" trend’s plastic equivalent: manufacturing single-piece "front-end carrier" modules for Electric Vehicles (EVs) to reduce assembly weight.

- LSR is the New Gold Rush: Liquid Silicone Rubber (LSR) injection molding is growing at 2.5x the rate of thermoplastics, driven by medical disposables and EV high-voltage connectors.

- The "Smart" Premium: Machines equipped with AI-driven melt-flow correction (adaptive process control) are commanding a 12–15% price premium over standard controllers, yet adoption rates in North America have doubled since 2023.

What Macro-Economic Threats Could Derail Production in 2025? (Supply Chain Challenges)

Semiconductors: While the crisis of 2022 has eased, "legacy chips" (used in machine controllers) remain tight in the plastic injection molding machines market. However, lead times for high-end European machines are still 6–8 months.

Steel Prices: Volatility in global steel prices directly impacts the manufacturing cost of the heavy two-platen machines (which are 80% steel by weight).

The Skills Gap: The most dangerous threat. The older generation of "Master Molders" who could tune a hydraulic machine by ear is retiring. The new workforce needs machines that tune themselves. This is driving the automation software market more than any other factor.

Where is the Real Market Growth Concentrated in Plastic Injection Molding Machines Market?

looking at revenue alone is misleading due to price inflation in raw materials (steel/cast iron). Following analysis would help understand the plastic injection molding machines market in better way.

Volume vs. Value Discrepancy

- Unit Shipments: The market is shipping approximately 145,000 units annually.

- The Asia Skew: China accounts for 60% of global unit volume but only 45% of global revenue. This indicates that while China is the volume factory, the high-margin, high-spec machinery (>$200k ASP) remains a stronghold of the DACH region (Germany, Austria, Switzerland) and Japan.

Segment Performance (YoY Growth 2024-2025)

- All-Electric Machines: +8.4% (The fastest growing segment).

- Two-Platen Hydraulic: +6.1% (Resurgence due to automotive infrastructure).

- Standard Hydraulic: -2.2% (The decline continues as servo-hydraulics replace standard pumps).

Hydraulic vs. All-Electric vs. Hybrid: Which Technology Wins the TCO War in the Plastic Injection Molding Machines Market?

Below is the definitive 2025 Efficiency Matrix.

| Feature | Hydraulic (Standard) | Servo-Hydraulic (Hybrid) | All-Electric |

| Energy Consumption | 0.65 – 0.85 kWh/kg | 0.35 – 0.45 kWh/kg | 0.20 – 0.28 kWh/kg |

| Precision (Repeatability) | ± 0.15% | ± 0.05% | ± 0.01% |

| Cooling Water Load | High (Oil cooling req.) | Medium | Zero/Low (No oil) |

| Noise Level | >75 dB | 68–72 dB | <65 dB |

| Maintenance Cost | High (Oil changes, leaks) | Medium | Low (Grease only) |

| Upfront Cost (Index) | 100 (Baseline) | 115 | 135 |

The "Hybrid" category is currently winning the Packaging sector in the plastic injection molding machines market. Thin-wall packaging requires high injection speeds (accumulators needed) that pure electrics struggle to match cost-effectively at high tonnages. However, for Medical and Electronics, All-Electric is now the non-negotiable standard due to cleanroom compliance (no oil mist).

How is the Death of the ICE Engine Reshaping Injection Molding Machines Market Growth? (Automotive Sector)

The transition from Internal Combustion Engines (ICE) to Electric Vehicles (EV) is a net-positive for the plastic injection molding machines market, but it changes what machines are bought. Currently, the market is losing demand for high-heat, under-the-hood parts (intake manifolds, fuel tanks) typically molded on standard hydraulic machines using glass-filled nylon.

However, At the same time, the market is seeing an explosion in "Smart Surfaces" and "Lightweighting."

- Polycarbonate Glazing: Replacing glass windows with plastic requires large, two-shot (2K) machines with "Spin-Stack" technology.

- Battery Casings: EV battery trays require massive tonnage (2,000T+) and fire-retardant materials.

- Interior: The dashboard is now a giant screen. This requires Cleanroom-grade molding for automotive displays—forcing automotive molders to buy machines previously reserved for the medical industry.

In 2025, 18% of all high-tonnage machine orders are specifically tagged for EV battery or sensor housing applications.

Why is Medical Molding the Ultimate High-Margin Fortress? (Healthcare Sector)

While the automotive industry holds prominence in the plastic injection molding machines market in terms of volume, but medical is the margin leader. This is mainly attributed to the move to ISO 13485 compliance. Which forces molders to retire older hydraulic machines. Wherein, it cannot have hydraulic fluid leaks in a Class 7 cleanroom.

- LSR Integration: Liquid Silicone Rubber is the material of 2025. Used in diaphragms, catheters, and wearable straps.

- Machine Impact: PIMMs must be retrofitted with specific LSR dosing units, cold-runner blocks, and vacuum systems to prevent air entrapment.

- The "Zero-Defect" Mandate: In medical molding, a reject rate of 1% is bankruptcy. This sector drives the adoption of AI-visual inspection systems integrated directly into the machine cell.

Can Thin-Wall Packaging Get Any Faster in the Plastic Injection Molding Machines Market? (Packaging & Consumer Goods)

The packaging sector in the plastic injection molding machines market is fighting a war on two fronts: Cycle Time and Sustainability.

- The Speed Limit: We have reached the physical limits of polymer cooling. Machines are now hitting cycle times of <2.0 seconds for 96-cavity closure molds.

- Tech Solution: Hybrid machines with accumulators (storing hydraulic energy for rapid bursts) are the only way to achieve the injection speeds (over 800 mm/s) required for thin-wall containers without burning out electric motors.

- The rPET Challenge: The mandate to use Recycled PET (rPET) or PP is wreaking havoc on machinery in the plastic injection molding machines market. Recycled material has inconsistent viscosity.

- Machine Response: OEMs are redesigning screws with barrier flight geometries and specialized coatings (bimetallic) to handle the abrasive nature of poorly filtered recycled plastics.

Are 'Smart Machines' a Marketing Gimmick or a Necessity? (Industry 4.0 & IIoT)

In 2020, "Industry 4.0" was a buzzword. In 2025, it is a survival mechanism.

- Euromap 77/83: These are the data exchange standards. If a machine cannot talk to the Manufacturing Execution System (MES) via OPC UA, Tier 1 suppliers will not buy it.

Smart Viscosity Correction: This is the "Killer App" of 2025.

The machine detects that the current batch of plastic is slightly thicker (viscosity change). Instead of making a short shot (defective part), the machine automatically increases the injection pressure and holding time in real-time within the same cycle.

- Impact: Reduces scrap rates by up to 40% when using recycled materials.

- Predictive Maintenance: Sensors now monitor screw wear and toggle lubrication levels, alerting maintenance teams 2 weeks before a failure occurs.

Who Are the True Market Leaders and Challengers in the Plastic Injection Molding Machines Market? (Competitive Landscape)

The market is consolidated at the top but fragmented at the bottom.

Tier 1 (Global Leaders):

- Haitian International: Unbeatable on price/performance for general purpose.

- Engel: The technology leader. Dominant in tie-bar-less and two-platen tech.

- Husky: The undisputed king of PET Preforms (Beverage packaging).

- Sumitomo (SHI) Demag: The leader in All-Electric precision.

Tier 2 (The Challengers):

- Arburg: Cult-like following in medical micro-molding.

- Nissei Plastic: Strong presence in optics and tactile automotive parts.

- Milacron: Strong in North America, particularly in large-tonnage infrastructure.

- Strategic Consolidation: We are seeing Japanese tech (electric motors) merging with European chassis designs to combat Chinese pricing pressure.

What is the Real Cost of Ownership Beyond the Sticker Price? (Price & TCO Analysis)

Stakeholders in the plastic injection molding machines market often ask: "Why pay $150,000 for an Electric when the Hydraulic is $100,000?"

The 5-Year TCO Calculation (350 Ton Machine):

- CAPEX: Electric (+$50k premium).

- Energy Savings: Electric saves ~$18,000 per year (at $0.12/kWh).

- 5-Year Savings: $90,000.

- Fluid Costs: Hydraulic requires ~400 liters of oil, changed annually + disposal fees + filters.

- 5-Year Savings: ~$12,000.

- Cooling Water: Electric generates less heat, reducing chiller load.

- 5-Year Savings: ~$8,000.

The electric machine saves $110,000 in OPEX over 5 years, paying off the $50k premium in just 2.2 years. In regions with higher energy costs (Germany, California), the ROI is under 18 months.

Segmental Analysis

By Clamping Force, Why is the 200–500 Ton Segment the Industry Workhorse? (Clamping Force Analysis)

The plastic injection molding machines market is bifurcating, but the middle remains the profit engine.

<200 Tons: The Precision Micro-Battle

- Share: 35% of the market.

- Driver: 5G/6G connectors, medical sensors, and wearable tech.

- Trend: "Micro-molding" machines (10–50 tons) are seeing renewed interest. OEMs like Sumitomo (SHI) Demag and Fanuc are dominating here with direct-drive motor technologies that offer instant acceleration.

200–500 Tons: The "Golden Mean"

- Share: 52.97% of the market.

- Driver: Automotive interiors and white goods (appliances).

This is the most competitive battlefield in the plastic injection molding machines market. Manufacturers are aggressively marketing "Tie-bar-less" technology (Engel) or "Two-platen compact" designs in this range to save factory floor space. In 2025, floor space utilization per square meter is a key KPI for molders.

>500 Tons: The Infrastructure Giants

- Driver: Logistics (pallets), Environmental bins, and EV lightweighting.

- Trend: The shift from Toggle systems to Two-Platen systems is near total in this segment. Two-platen machines have a smaller footprint and better tonnage linearity, essential for the massive molds used in automotive bumpers.

By Machine Type, Hydraulic Systems Retain Command Through Cost-Efficiency and High-Force Capabilities

Hydraulic injection molding machines maintain their stronghold in the plastic injection molding machines market due to their unmatched ability to generate high clamping forces at a lower capital cost compared to all-electric alternatives. In 2025, industry leaders like Haitian International reported that their servo-hydraulic "Mars" series continued to be a primary revenue driver, contributing significantly to their delivery of over 53,000 units in 2024.

While electric machines are growing, hydraulic systems remain the standard for molding large, heavy-duty automotive and industrial parts where raw power is non-negotiable. Major manufacturers such as ENGEL have reinforced this dominance by integrating energy-saving servo-hydraulics in their 2025 heavy-tonnage "duo" series, offering the power of hydraulics with improved energy efficiency. This segment’s leadership is further solidified by the construction and heavy machinery sectors, which rely exclusively on the durability and high-pressure capabilities that only hydraulic systems can consistently provide.

By Machine Structure, Horizontal Configurations Lead Global Manufacturing Standard for Automation and Speed

Horizontal injection molding machines command over 75% of revenue of the plastic injection molding machines market because they remain the global standard for high-speed, automated mass production. Unlike vertical machines, which are niche solutions for insert molding, horizontal systems allow for gravity-assisted part ejection and seamless integration with robotic automation cells—a critical requirement for modern "Lights Out" manufacturing factories.

In 2025, major equipment suppliers like Husky Injection Molding Systems emphasized that their horizontal platforms are the primary choice for the packaging and medical sectors, where cycle times are measured in fractions of a second. Operational reports from 2025 show that new factories in Southeast Asia and Mexico are almost exclusively outfitting floor space with horizontal setups to maximize throughput.

This structural dominance is unchallenged in high-volume applications, where the ergonomics of horizontal clamping units facilitate rapid mold changes and continuous operation.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

By Industry, Automotive Sector in the Plastic Injection Molding Machines Market Drives Demand Through EV Lightweighting and Interior Customization

The automotive industry leads the market by contributing over 28% of revenue, fueled by an aggressive push for vehicle lightweighting and the electrification of global fleets. As of 2025, carmakers are replacing traditional metal components with high-performance engineered plastics to extend Electric Vehicle (EV) range, directly spiking demand for large-tonnage molding capacity.

ENGEL’s showcase at K 2025 featured massive 5,500-ton machines specifically designed for producing large automotive panels, underscoring the sector's pivotal role. Additionally, 2025 production forecasts from major suppliers like Magna and Faurecia reveal a heavy reliance on injection molding for smart interior surfaces and sensor-integrated bumpers.

The plastic injection molding machines market’s requirement for zero-defect precision parts has forced machinery OEMs to tailor their most advanced, high-margin innovations specifically for automotive clients, ensuring this sector remains the primary engine of market growth.

To Understand More About this Research: Request A Free Sample

China vs. Europe vs. North America: Who Controls the Supply Chain?

Asia leads volume (65% share) and capture over 43% market share of the plastic injection molding machines market, Europe owns premium tech, and North America drives reshoring.

China (The Volume King):

- Dominance: Haitian International shipped over 120,000 units in 2025 (per company filings), holding ~45% global market share by volume—dwarfing competitors amid a 7% industry growth rate.

- Shift: No longer just "cheap," Chinese OEMs like Haitian and Yizumi are exporting premium all-electric models (e.g., Jupiter series) to SE Asia and South America, undercutting Japanese pricing by 20-30% while matching energy efficiency (up to 80% less power draw vs. hydraulics). This has captured 25% of Brazil's market since 2023.

Geopolitical tensions are accelerating "China+1" strategies. At the same time, Vietnam imports surged 40% YoY, but Haitian in the plastic injection molding machines market counters with localized assembly plants, retaining cost leadership despite US tariffs hitting 25% on key components.

Europe (The Tech Lead):

- DACH Core (Engel, KraussMaffei, Arburg): They own the "System Solution," bundling robots, molds, and conveyors into certified cells—essential for medical (ISO 13485 compliance) and automotive Tier 1s needing 99.9% uptime. Engel alone delivered 15,000+ integrated lines in 2025.

Hybrid tech reigns supreme in the Europe plastic injection molding machines market. For instance, Arburg's ALLROUNDERs with AI predictive maintenance cut downtime by 30%, per VDMA data. Europe's edge faces pressure from energy costs (up 15% post-2024), pushing sales of low-energy machines—but they command 2-3x premiums over Asian rivals in high-precision segments like pharma packaging.

North America (The Reshoring Hub):

USMCA Impact: "Made in USA" mandates for EV credits (IRA Section 30D) are fueling $5B+ in US molding investments since 2023, per Reshoring Institute stats—sparking a 20% technician shortage and booming demand for intuitive interfaces like Husky's Synergy controllers (touchscreen AI diagnostics).

Milacron and Wittmann Battenfeld are riding the wave with modular "plug-and-play" cells tailored for EV battery housings. North America's market grew 12% YoY to $4.2B in 2025. However, supply chain bottlenecks in resins (e.g., PP shortages) expose vulnerabilities, with 60% of new capacity still reliant on imported Asian components.

Top Players in Plastic Injection Molding Machines Market

- Arburg GmbH & Co. KG

- Borche North America Inc.

- Chen Hsong Holdings Limited

- Dongshin Hydraulic Co. Ltd.

- Dr. Boy GmbH & Co. KG

- Engel Austria GmbH

- Fu Chun Shin Machinery Manufacture Co. Ltd.

- Haitian International Holdings Limited

- Hillenbrabd, Inc.

- Husky Injection Molding Systems

- Krauss Maffei Group

- Shibaura Machine Co Ltd.

- Sumitomo Heavy Industries

- The Japan Steel Works

- Ube Industries, Ltd.

- Other Prominent players

Market Segmentation Overview:

By Machine Type

- Electric

- Hydraulic

- Hybrid

By Clamping Type

- 0-200 Ton Force

- 201-500 Ton Force

- Above 500 Ton Force

By Machine Structure

- Vertical Injection Molding Machines

- Horizontal Injection Molding Machines

By Secondary Process

- Ultrasonic Welding

- Pad Printing

- Silk Screen

- Job Assembly

- Hot Plate Welding

- Others

By Sales Channel

- Direct

- Distributor

By Industry

- Automotive

- Electronics and Telecommunication

- Healthcare

- Packaging

- Aerospace

- Food & Beverage

- Construction

- Consumer Goods

- Others

By Region

- North America

- The U.S.

- Canada

- Mexico

- Europe

- Western Europe

- The UK

- Germany

- France

- Italy

- Spain

- Rest of Western Europe

- Eastern Europe

- Poland

- Russia

- Rest of Eastern Europe

- Western Europe

- Asia Pacific

- China

- India

- Japan

- Australia & New Zealand

- South Korea

- ASEAN

- Rest of Asia Pacific

- Middle East & Africa (MEA)

- Saudi Arabia

- South Africa

- UAE

- Rest of MEA

- South America

- Argentina

- Brazil

- Rest of South America

FREQUENTLY ASKED QUESTIONS

The market was valued at US$8.26 billion in 2025. It is projected to reach US$14.28 billion by 2035 at a CAGR of 5.63% during 2026-2035. Growth stems from EV lightweighting and all-electric machines.

This segment holds 52.97% market share. It serves as the workhorse for automotive interiors and appliances. Tie-bar-less and two-platen designs optimize factory floor space.

Horizontal machines command 75.33% revenue. They enable high-speed automation with gravity-assisted ejection. Robots integrate seamlessly for packaging and medical applications.

Automotive contributes over 28% revenue. The EV shift boosts >2,000-ton orders for battery casings. Now 18% of high-tonnage sales target sensor housings and lightweight panels.

Asia-Pacific controls 43% share. China's Haitian ships 120k+ units yearly at 20-30% lower prices. Localized plants counter Vietnam's China+1 surge with premium exports.

All-electric machines grow fastest at +8.4% YoY. They consume 0.20 kWh/kg versus hydraulic's 0.65. The $50k premium pays back in 1.8 years with $110k 5-year OPEX savings.

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |